Climate Strategy

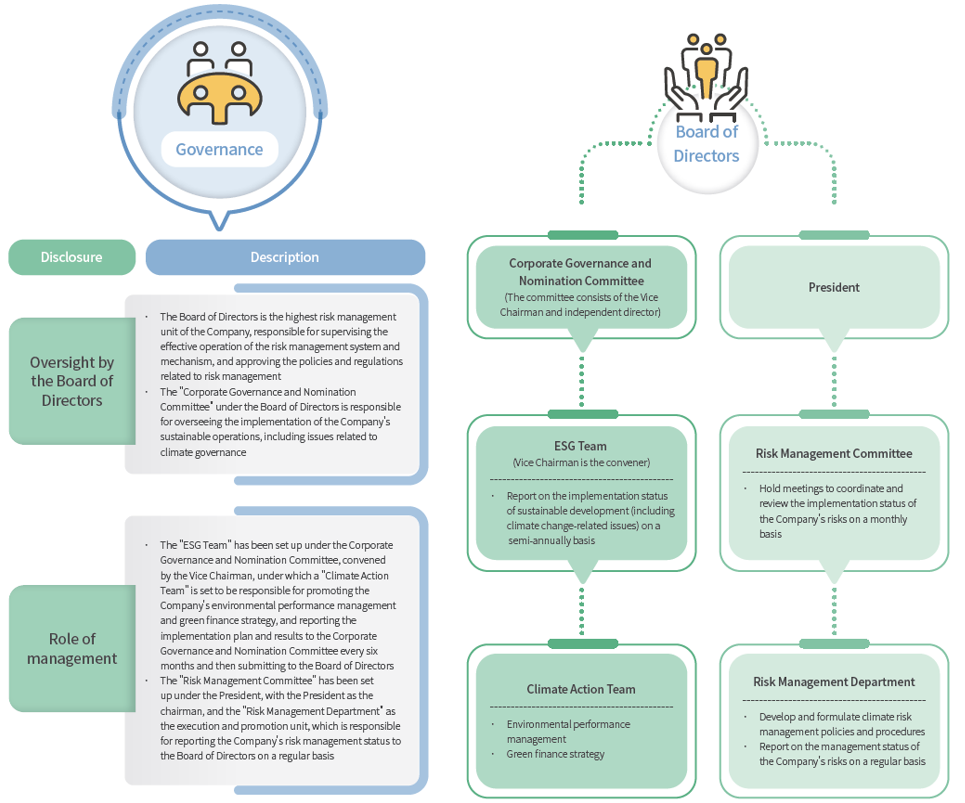

Governance

World Economic Forum released "Global Risk Report" in January 2023, in which it showed that in a world of unbalanced geopolitical and economic environment, the increased living cost would come into accelerated deterioration. However, the greatest challenge in next ten years mainly refers to crisis in environmental and social aspects, especially environmental risk. Compared with the ten risks in 2022, the environmental risks increased not only in quantity from 5 to 6, but also in severity, and more emphasis was laid on importance of taking actions to cope with climate change.

In response to global climate action, KTB has became a supporter of Task Force on Climate-related Financial Disclosure(TCFD) in July 2021, and with reference to the TCFD framework, KTB made disclosure in 2021 sustainability Report in terms of governance, strategy, risk management, indicators and goals. In 2022, KTB continued to improve its mastery of the impact of climate risks on finance, adopted the Network for Greening the Financial System (NGFS) and the Representative concentration pathways (RCPs) of the 5th Assessment Report (AR5) of the Intergovernmental Panel on Climate Change (IPCC), as well as the "Scenario Analysis of Climate Changes by Domestic Banks in 2022" released by Taiwan competent authority, to implement and deepen management and information transparency of climate risks.

Strategy and Risk Management

KTB's climate-related management strategy mainly focuses on three aspects, which is taken as the direction for optimization year-by-year:

■Manage climate-related risks, including physical and transition risks

■Manage the impact of the Company's operations on the climate

■Support customers in their transition to a low-carbon economy with financing or investment products

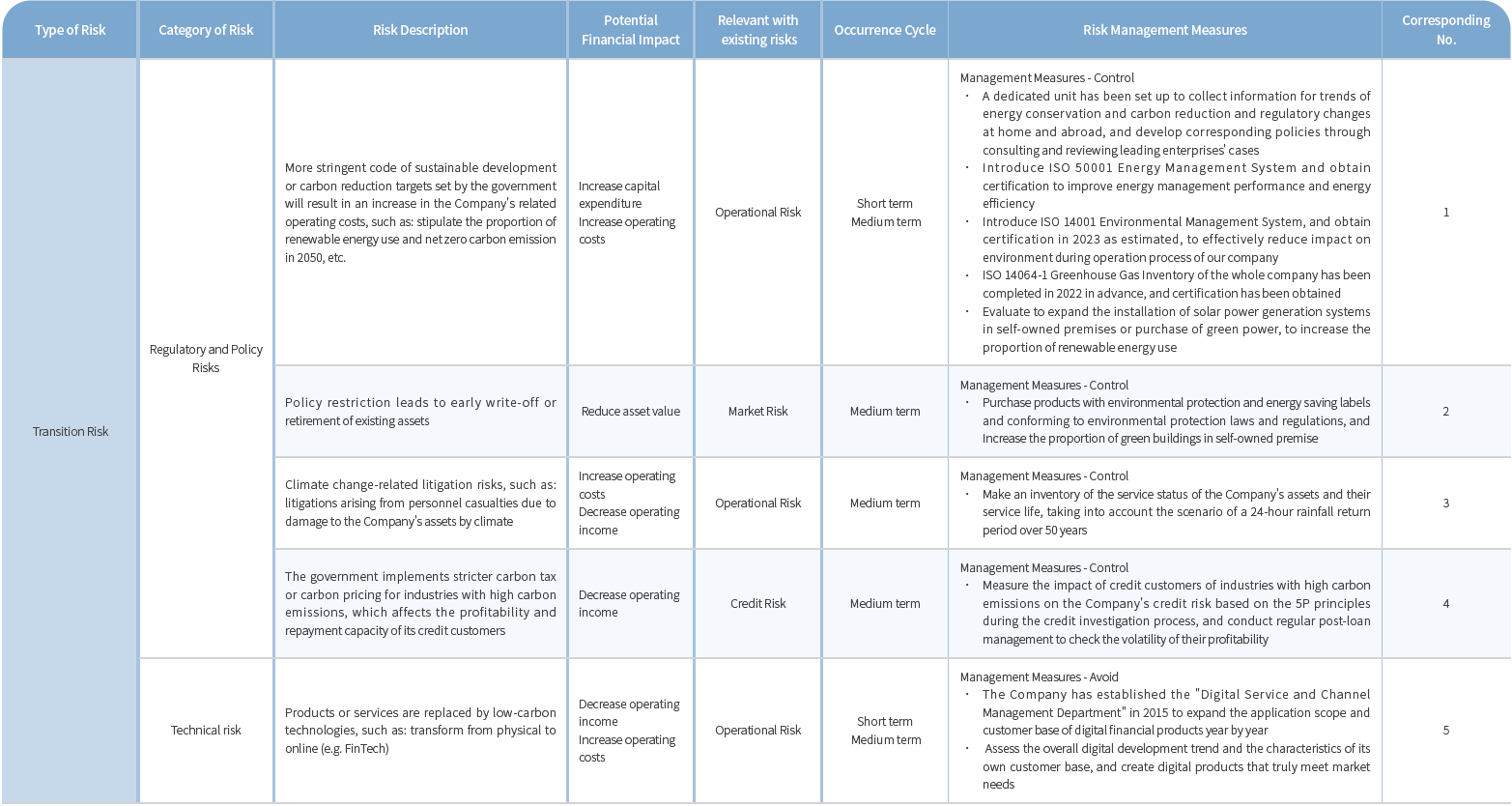

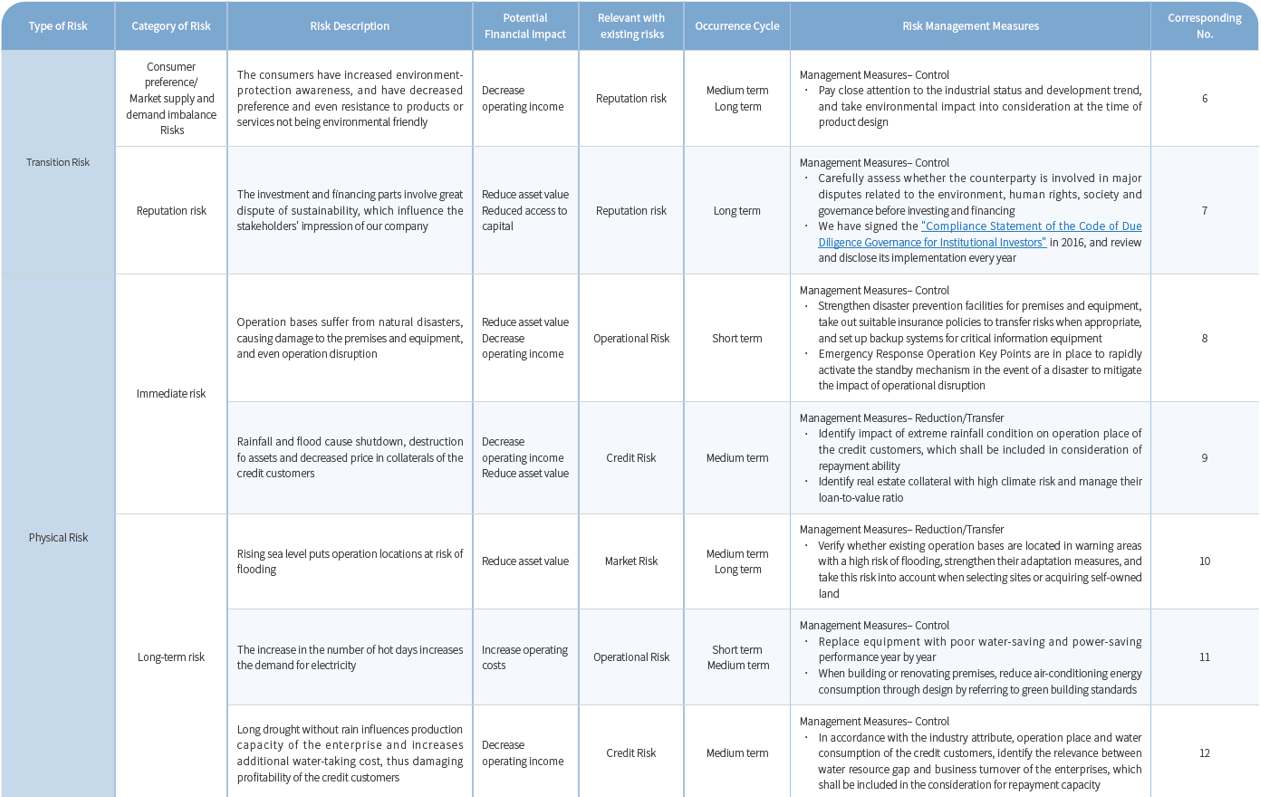

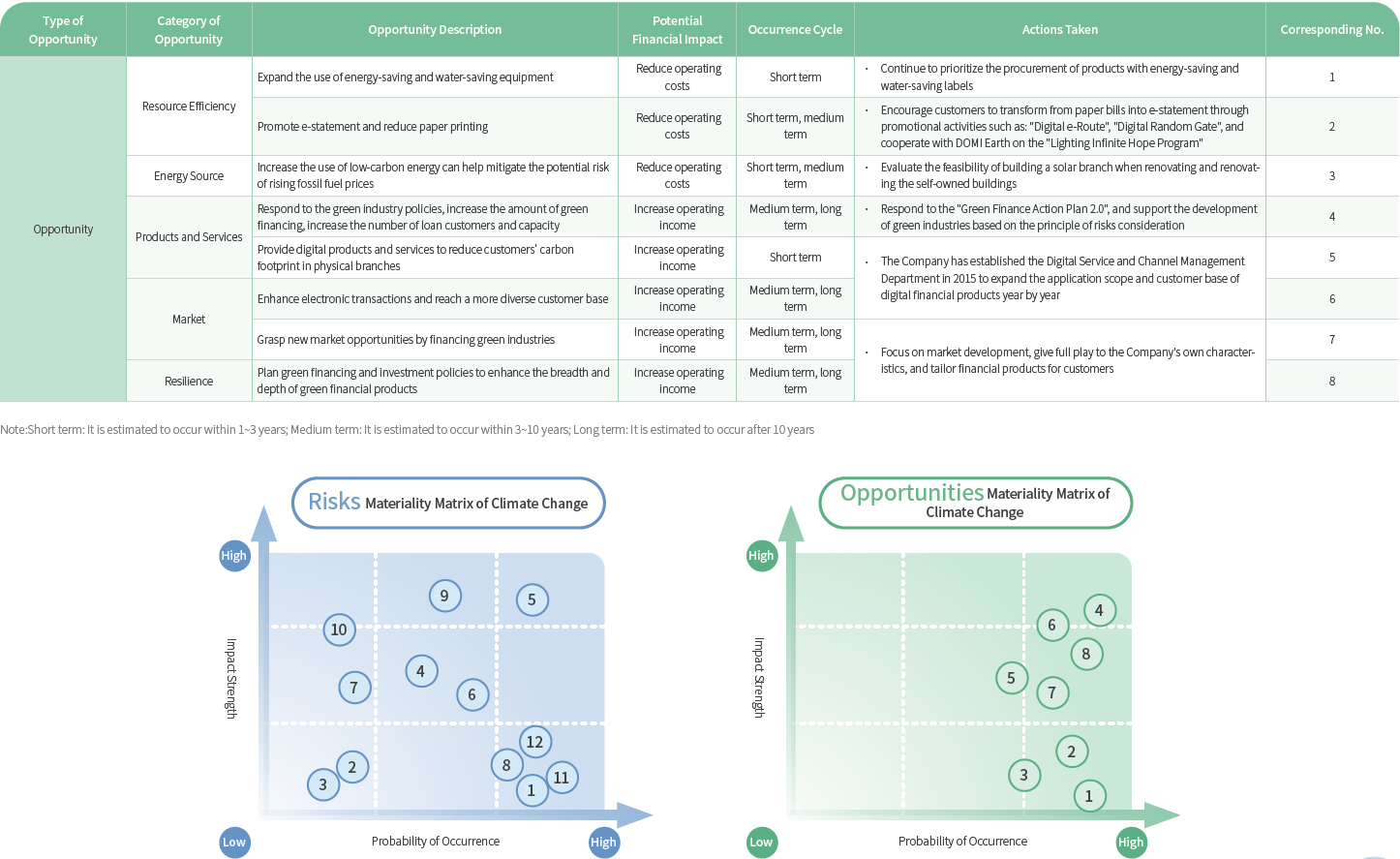

Climate Risks and Opportunities

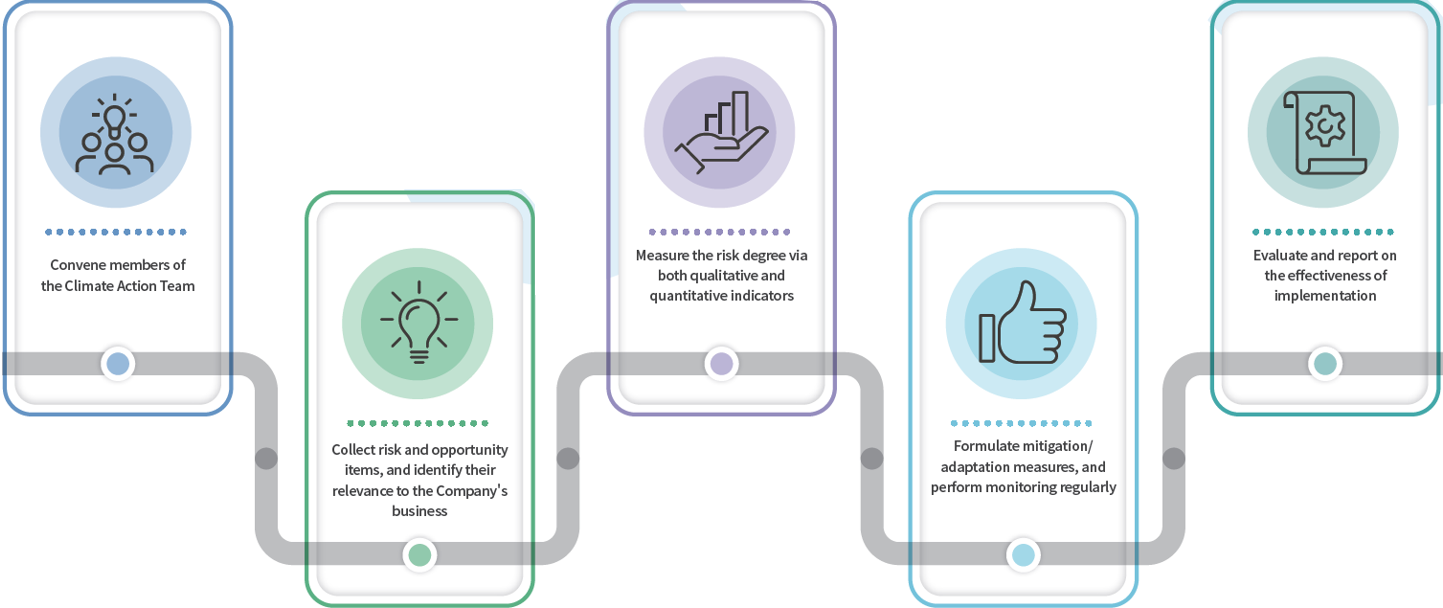

According to the framework of the TCFD proposal, the Company has identified a total of 12 climate risk items and 8 climate opportunity items associated with the Company, and invited members of the Climate Action Team to assess the degree of impact on the Company's business, strategy or financial planning and the possibility of occurrence, and draw up the Company's risk opportunity materiality matrix.

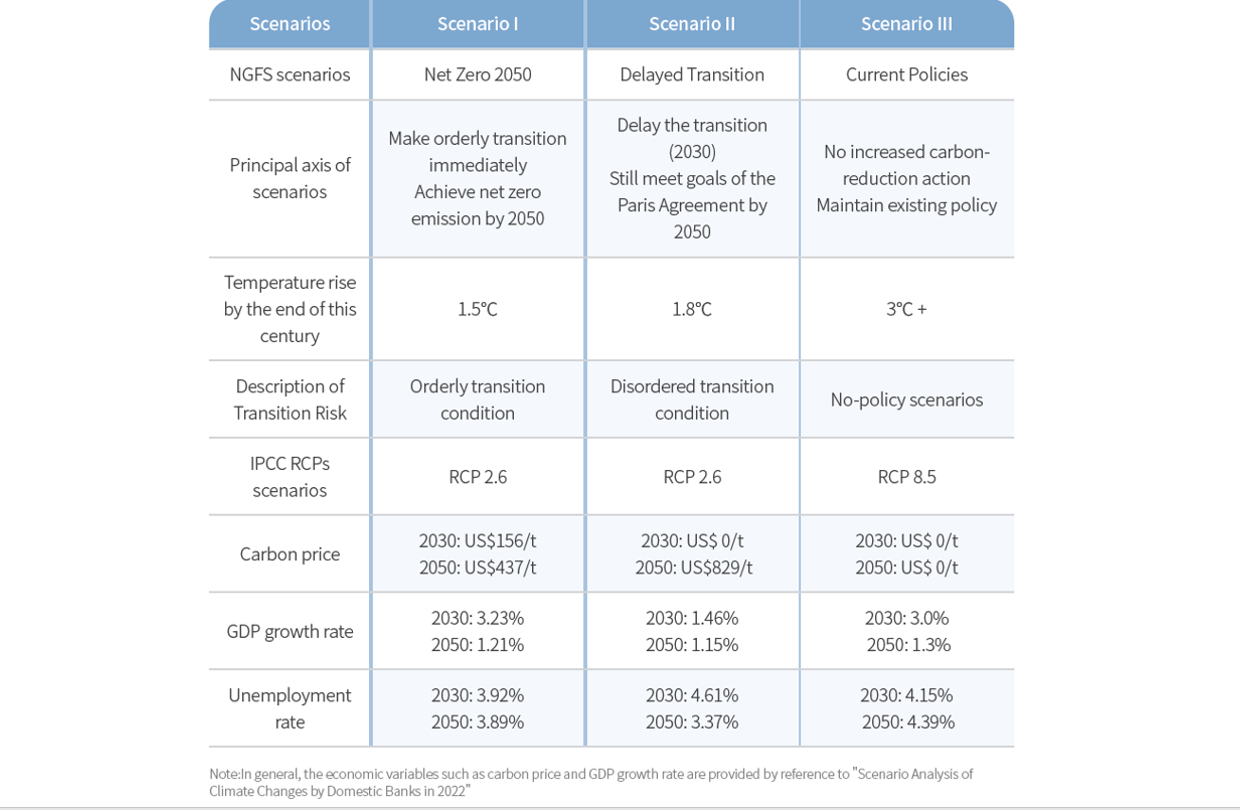

Scenario setting

Taking the scenario framework of the Network for Greening the Financial System (NGFS) in 2021, KTB selected Net Zero 2050, Delayed Transition and Current Policies as the main basis for transition scenario factors, then produce physical risk related factor using IPCC's RCPs scenario, and then make corresponding integration.

Climate risk scenario setting of KTB in 2022 was as follows:

Scenario Analysis Result

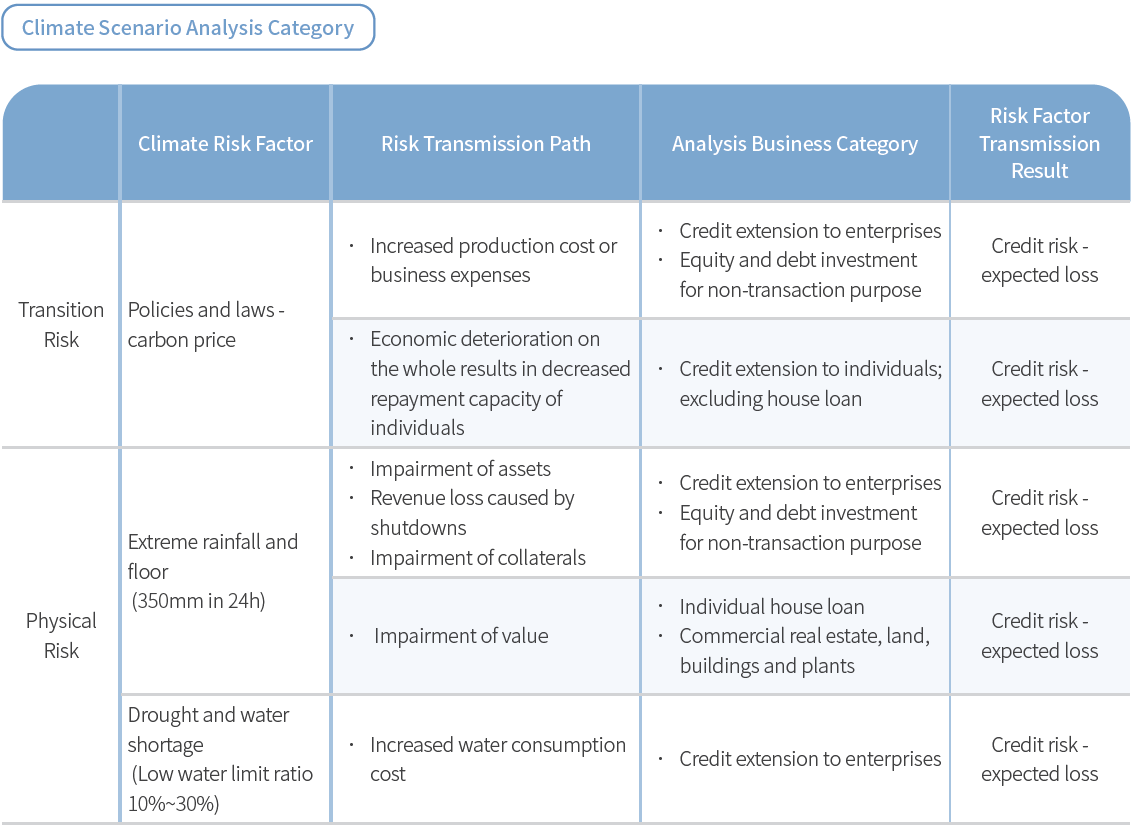

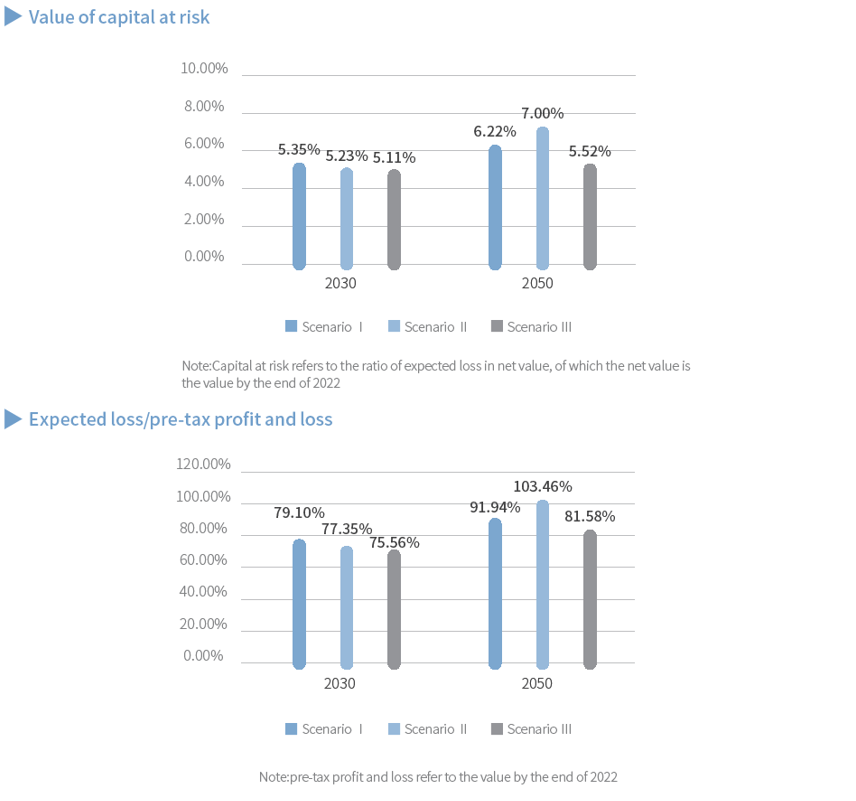

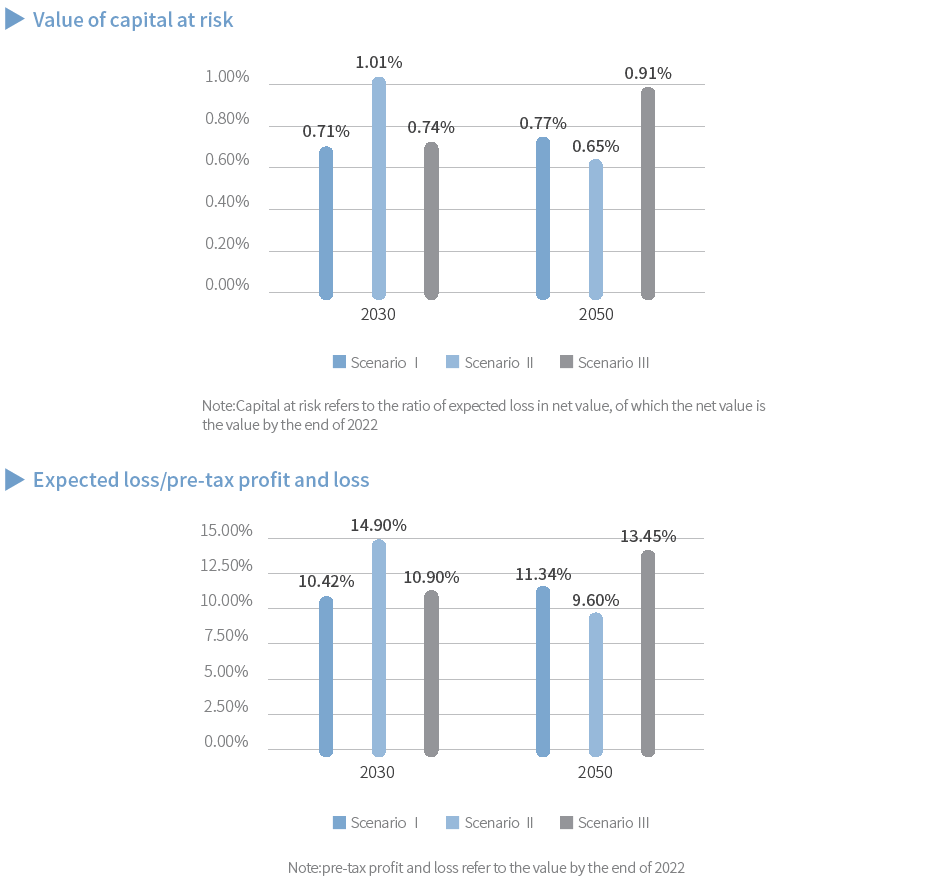

Under the above climate scenario architecture, we used post pressurization loss change circumstance of the credit risk parameters i.e. Probability of Default (PD) and Loss Given Default (LGD) evaluating domestic and foreign credit, domestic foreign-currency securities and equity investment of KTB, and demonstrated the evaluation result using capital at risk.

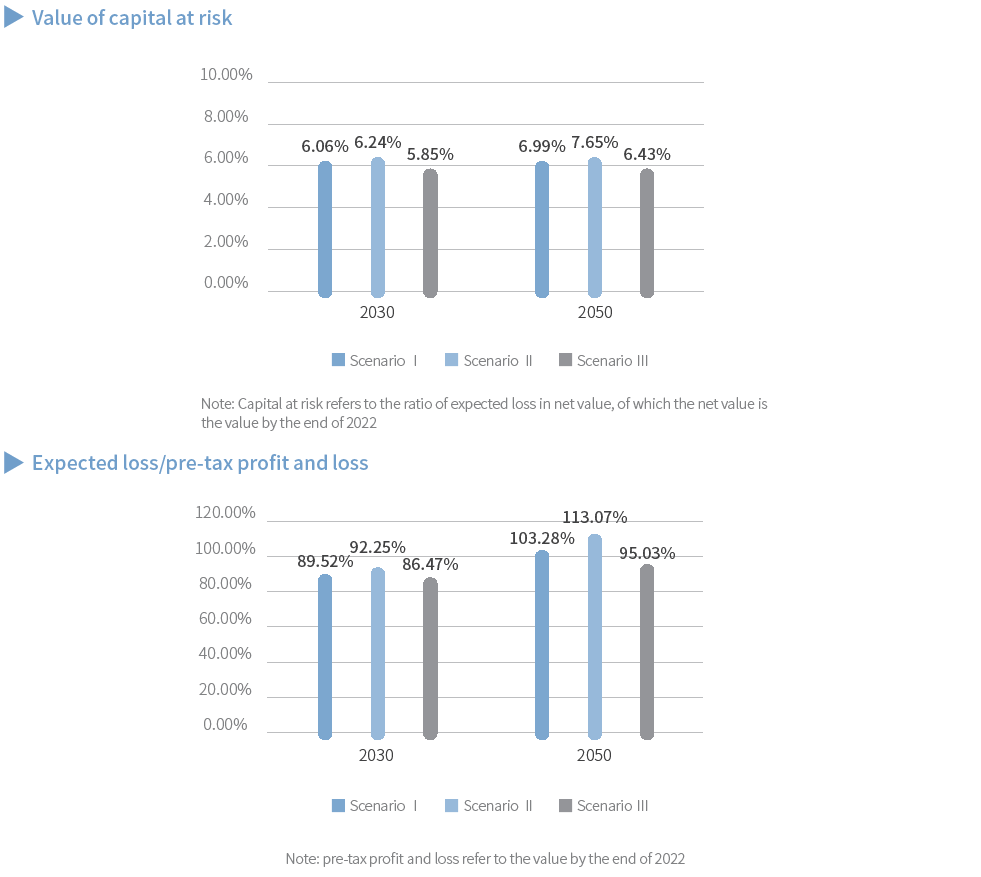

It is discovered that, expected loss under various scenarios in 2050 is higher than that in 2030, showing that the climate risk becomes intensified with time going on. By making comparison of the difference in different scenarios, both Scenario I and Scenario II adopted transition action, but in Scenario II, it is assumed that transition step in preliminary stage is gentle, and relatively active transition strategy is taken until 2030, therefore, in 2030, Scenario II needs to suffer from a higher transition risk than Scenario I, and with time going on to 2050, it will suffer from a higher physical risk impact as well.

General Corporate Credit Business

Scenario analysis result in 2030 showed that, although both Scenario I and Scenario II are confronted with transition risk, Scenario I has slightly higher credit risk than Scenario II, which is mainly due to that the impact brought by policy change has shown appearance gradually, however, by 2050, Scenario I will have slightly lower credit risk than Scenario II.

In 2050, capital at risk of general corporate credit business under all scenarios is higher than that in 2030, especially Scenario II. It is shown that under disordered transition, there are both physical risk and higher transition risk in 2050.

Individual Credit Business

In 2030, capital at risk of Scenario II is significantly higher than Scenario I. This is mainly due to that both Scenario I and Scenario II have transition action, but in Scenario II, it is assumed that relatively active action begins from 2030, and the impact of policy change on overall economy will always be the maximum during 5-10 years from the beginning of transition, and then decreased year by year, besides, the more active the action, the greater impact on overall economy. And also for this reason, the individual credit business in 2030 is easy to suffer from a higher credit risk under the condition of low economic growth rate and high unemployment rate.

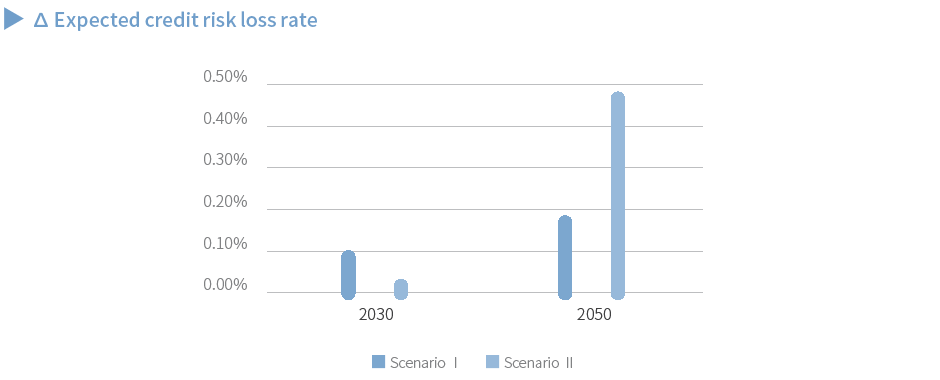

Investment business for non-transaction purpose

In 2030, expected credit risk loss rate (EL%) of Scenario I is higher than Scenario II, with an increase of 10 basis points (0.01%) on average compared with the benchmark, which mainly reflects the impact brought by policy adjustment within a short term. In 2050, EL% of Scenario II is higher than Scenario I, with an increase of 42.2 basis points on average, which reflects the increasingly expanded impact brought by physical risk with time going on.

Performance Indicators and Objectives

Please refer to the tabbed path: Home / Sustainability / Environment / Sustainable Operating Environment (https://esg.ktb.com.tw/sustainability/sustainable-environment).